Get Advanced Insights on Any Topic

Discover Trends 12+ Months Before Everyone Else

How We Find Trends Before They Take Off

Exploding Topics’ advanced algorithm monitors millions of unstructured data points to spot trends early on.

Keyword Research

Performance Tracking

Competitor Intelligence

Fix Your Site’s SEO Issues in 30 Seconds

Find technical issues blocking search visibility. Get prioritized, actionable fixes in seconds.

Powered by data from

Latest Blog Posts

Featured Case Studies

See what's trending before everyone else

Each week, we'll send you our best Exploding Topics. Plus, expert insight and analysis.

5 Important Wealth Management Trends (2024-2026)

You may also like:

The wealth management industry is experiencing rapid change.

New technologies, new investment opportunities, and a new crop of financial advisors are all disrupting the status quo.

There’s also uncertainty as wealth changes hands and investors look to control more of their investments through apps and automation.

We’ve listed six trends that are impacting the wealth management industry today, and we expect these changes to have a sizable impact on the future of investing in the next decade.

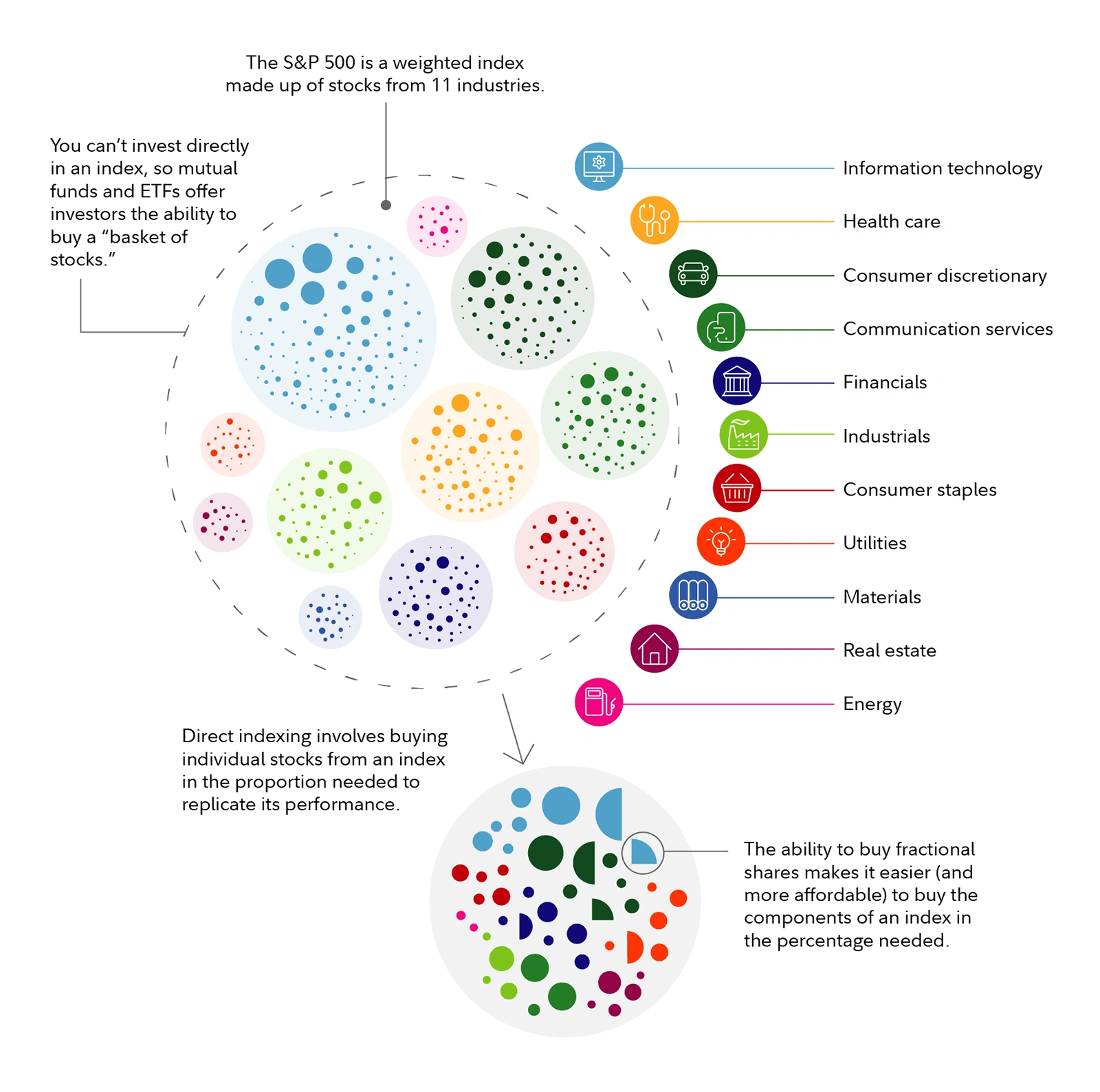

1. Investors find the customization they want with direct indexing

One of the most impactful trends we’re seeing in wealth management is investors seeking out customized investment solutions. Direct indexing is one solution that makes that possible.

The direct indexing market was valued at $400 billion in 2021 and is still growing at an incredible rate, up to $730.5 billion by 2026.

This investment strategy involves directly buying the individual stocks that make up an index at the appropriate weights.

It provides more control and autonomy for the investor than owning a mutual fund or ETF. It also gives investors the opportunity to tax-loss harvest individual positions, which can increase returns by 1% per year.

In the past, direct indexing was an investment strategy reserved for the wealthiest individuals. However, fractional shares trading and zero-commission trades have led more investors to pursue this strategy.

Although direct indexing would’ve resulted in expensive fees and commissions in the past, zero-commission stock trading platforms have erased that burden.

In fact, many brokers are jumping on this trend to offer direct indexing.

One report predicts there will be $1.5 trillion in direct indexing managed accounts by 2025. That’s compared to $350 billion in 2020.

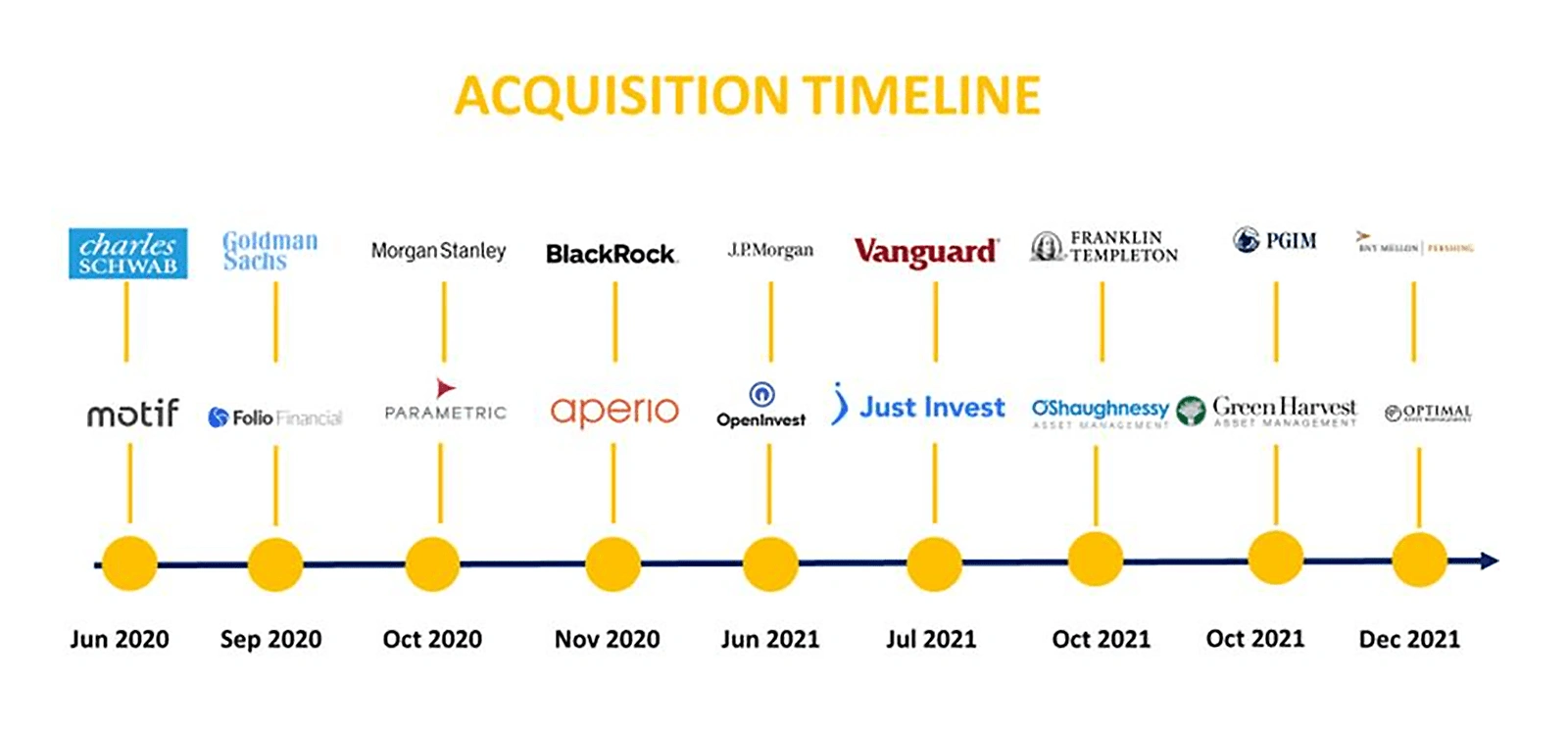

Morgan Stanley, BlackRock, Vanguard, Fidelity, and Schwab have all acquired direct indexing firms in recent years.

Several big-name firms are now offering direct indexing as part of their wealth management strategy.

Investors looking at Schwab will need at least $250,000 to invest in most of the company’s direct indexing services. The pricing starts at 0.40%.

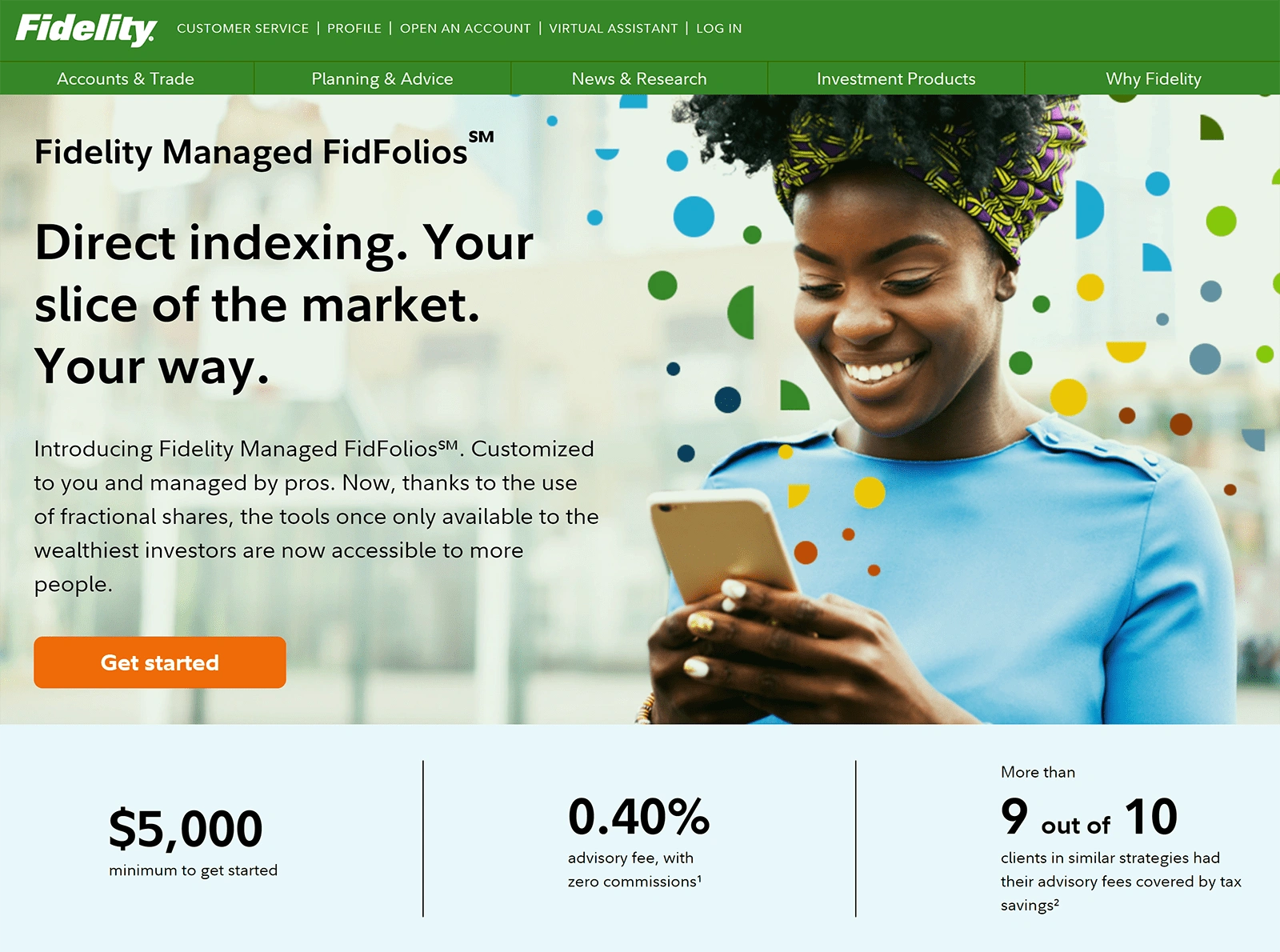

Fidelity’s direct indexing services with partial customization options require a $5,000 investment minimum and also charge a 0.40% advisor fee.

Fidelity, which handles $11.5 trillion in assets, began offering direct indexing in March 2022.

2. Wealth transfer creates a new generation of investors

In the next few decades, the “most significant intergenerational wealth transfer in history” will be happening.

As Baby Boomers hand down inheritance to younger generations, many people who have been living in the middle class will soon have a substantial amount of income available to invest.

One consulting firm, Cerulli Associates, expects $84 trillion of wealth to transfer through to 2045.

The New York Times estimates the wealth transfer will be much smaller, only $15 trillion.

How will these younger generations choose to manage their wealth? Predictions vary, but have one common thread: they’ll do it much differently than their parents did.

One survey found that 80% to 98% of heirs will not stick with their parent’s financial advisor.

It seems they have a good reason to go.

A 2021 survey showed that only 38% of wealth managers say they’re able to understand and cater to the unique needs of millennials.

Younger generations aren’t afraid to get second opinions, either, even from a computer.

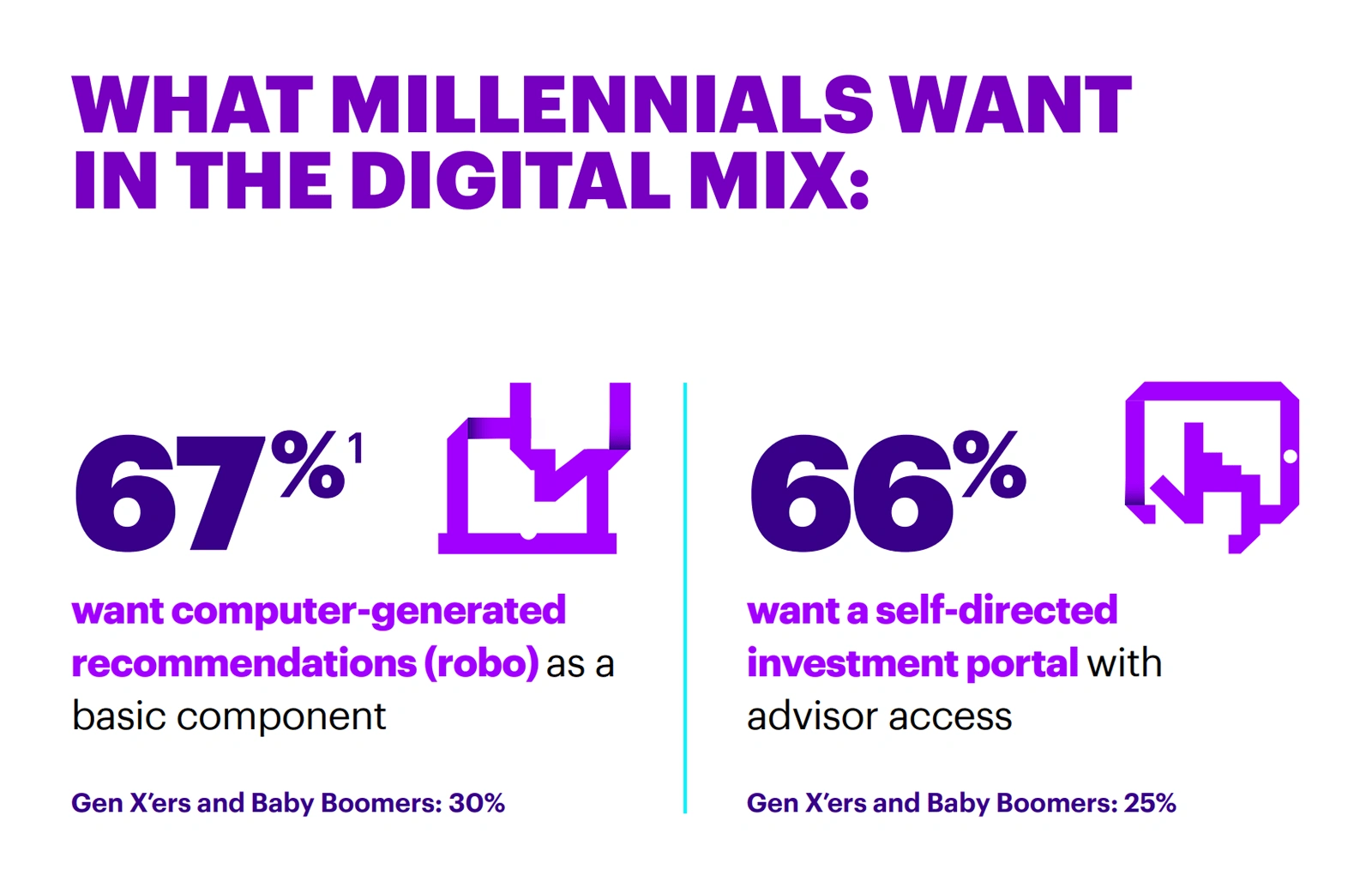

A study from Accenture showed that 67% of millennials want computer-generated wealth management recommendations.

Recent surveys show that Millennials and younger generations aren’t satisfied with the traditional tools and resources used in wealth management.

In fact, Millennials are twice as likely as Baby Boomers to use robo-advising, a market that’s expected to reach $1.2 trillion in 2024.

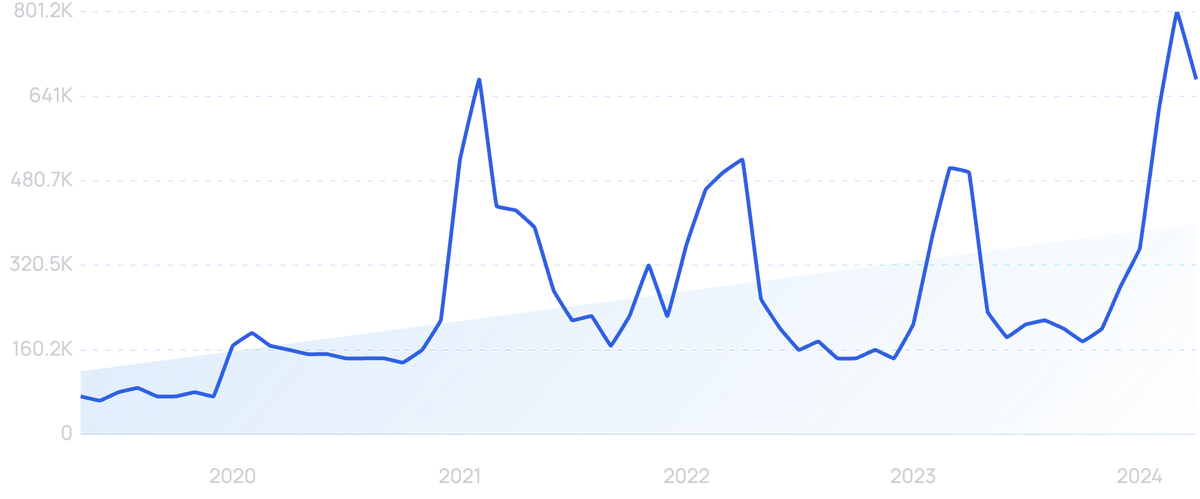

Wealthsimple is one company that’s offering financial solutions that appeal specifically to this generation.

Search volume for “Wealthsimple” peaked during the early days of the pandemic but has still grown over 5 years.

The company offers robo-advising that automatically rebalances and reinvests dividends. Plus, there are human advisors available, if needed.

Many Millennials are already drawn to this platform because you can invest with as little as $1.

Overall, wealth management advisors are preparing for the generational wealth shift and taking steps to understand these new, younger clients.

This includes things like focusing on financial literacy, emphasizing tax burdens, building relationships, and hyper-personalizing offerings.

3. Money pours into sustainable investing

In today’s world, investors are considering more than just profits as they choose where to put their dollars. They’re looking at environmental, social, and corporate governance (ESG) factors, too.

In sustainable investing, people are looking to drive profits while ensuring a positive impact on society. For example, these investors avoid oil and gas companies and invest in clean energy companies instead.

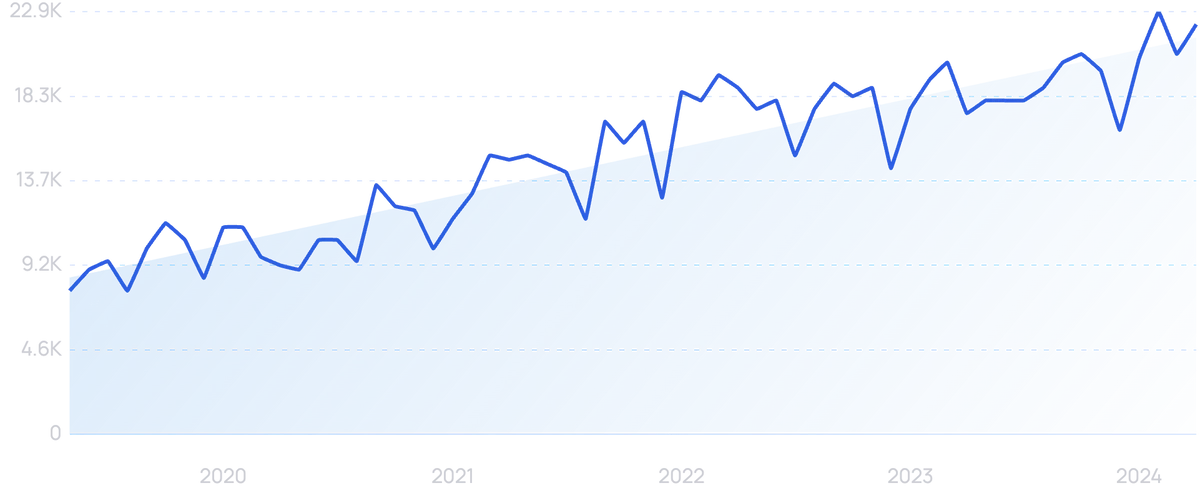

Search volume for “sustainable finance” is up 185% over the past 5 years.

In 2018, there was $12 trillion in US assets invested using sustainable investment strategies. By 2020, that number was $17.1 trillion, an increase of 42%.

Globally, ESG assets are expected to top $53 trillion by 2025.

Reuters reports that $649 billion went into ESG-focused funds in 2021. That’s up from $542 billion in 2020.

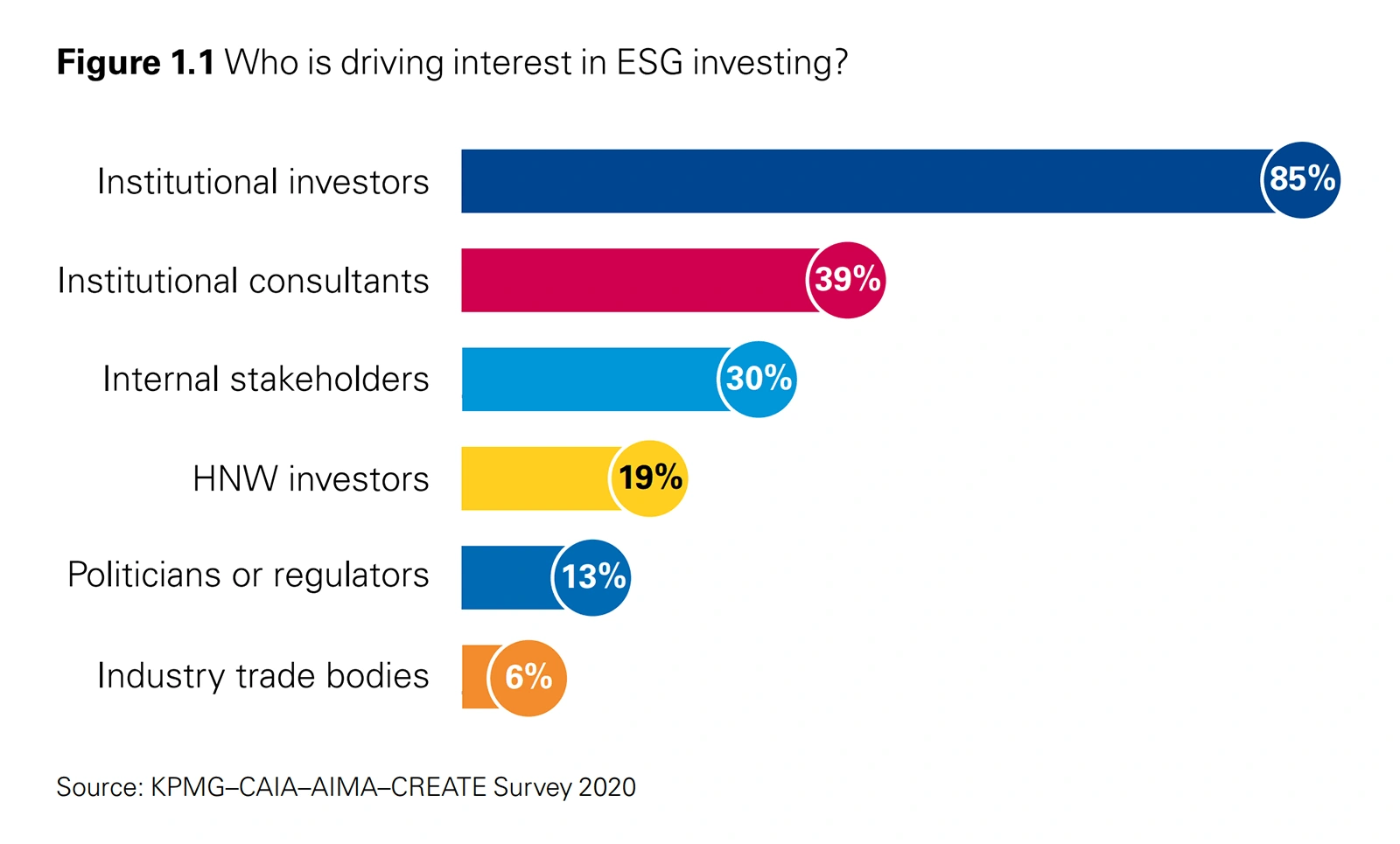

KPMG reports that institutional investors are driving the interest in sustainable investing, but other stakeholders are playing a part, too.

A KPMG survey showed that hedge fund managers say institutional investors are driving the interest in ESG investing.

The CFA Institute reports that 85% of investment professionals in its organization use ESG factors as they consider investments. That represents a 12% increase since 2017.

To guide investors, many organizations and individual companies are offering reports on ESG initiatives.

The MSCI ESG Ratings list the ESG performance of nearly 3,000 companies. They rank companies according to implied temperature rise, decarbonization targets, and labor management.

Search volume for “MSCI” has grown by 125% in the past 5 years.

Still, many investors struggle to measure ESG impact.

One report stated that 80% of global investors find it challenging to manage ESG investments and call “greenwashing” a real obstacle.

Investors are struggling to define what ESG really means for their firms and their clients.

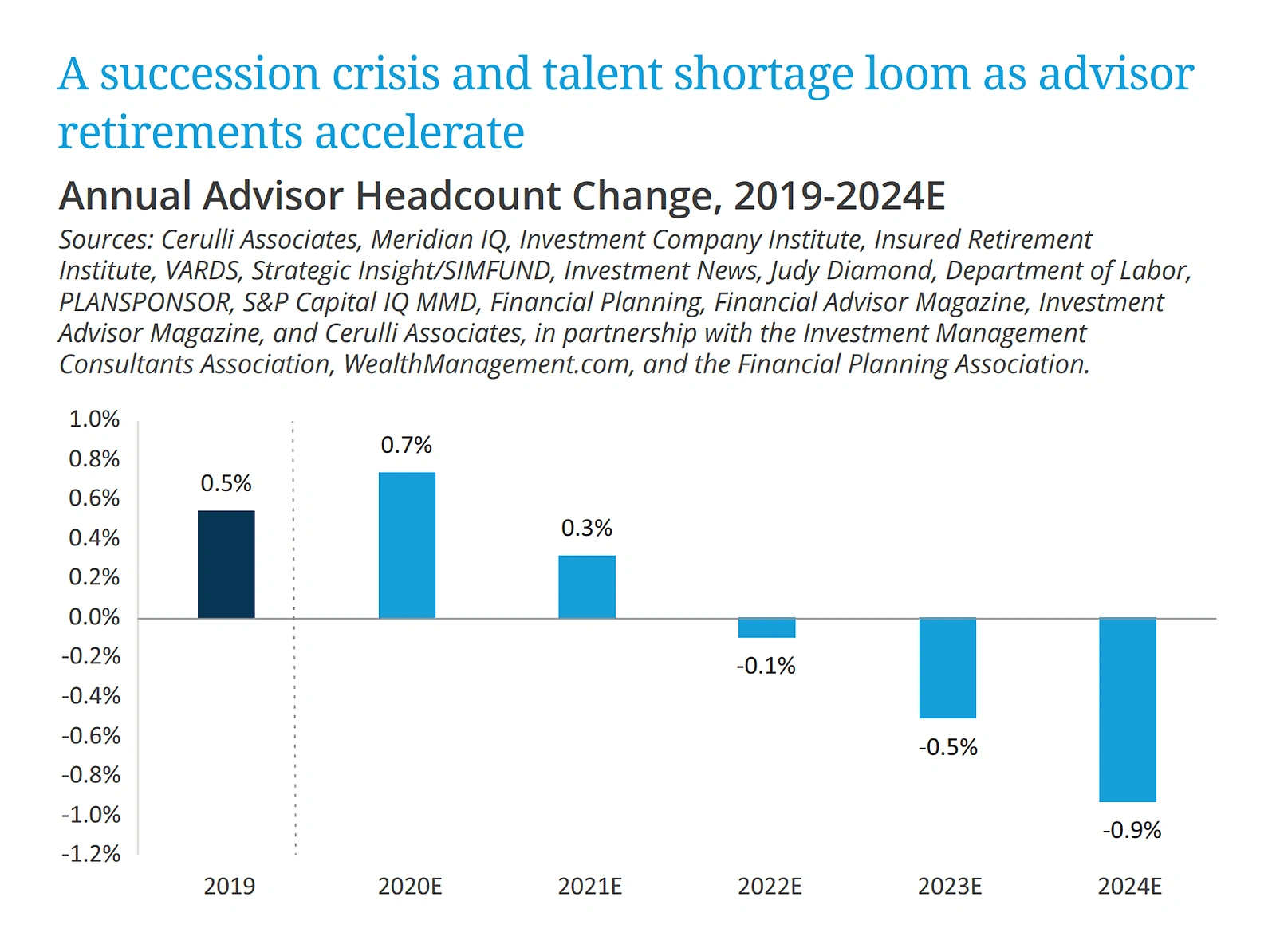

4. Retiring advisors put recruitment pressure on wealth management firms

In the next 10 years, data shows that up to 103,000 current financial advisors will retire. That represents 40% of total advisors.

The number of financial advisors is expected to decline substantially.

Right now, 44% of registered investment advisors are older than 60. Only 11% are under 40.

Even before they retire, aging advisors can be resistant to using new tools and adopting a hybrid model of advisory that adds AI-based recommendations to their expertise.

How will wealth management firms address this trend?

Some have succession plans in place, but many do not. Estimates vary on this data point.

One study from 2017 showed that only 37% of firms have a succession plan. However, another study put that number at 64%.

Estimates show the wealth management industry needs approximately 240,000 new advisors to step up in order to maintain current service levels.

This is leading many firms to amp up recruitment focused on hiring younger, more diverse staff members.

As more firms are emphasizing hiring advisors from historically underrepresented groups, we’ve seen more firms turning to diversity and inclusion officers.

Data from 2019 shows women make up 33% of all financial advisors. African Americans make up just 8% and Hispanics only 7%.

However, the number of African-American and Hispanic-certified financial planners increased by 12% that year, the highest yearly increase ever.

Often, students graduating college with degrees related to financial planning have multiple job offers before they walk across the stage.

Some firms report going as far as to hire gig workers to fill the gaps.

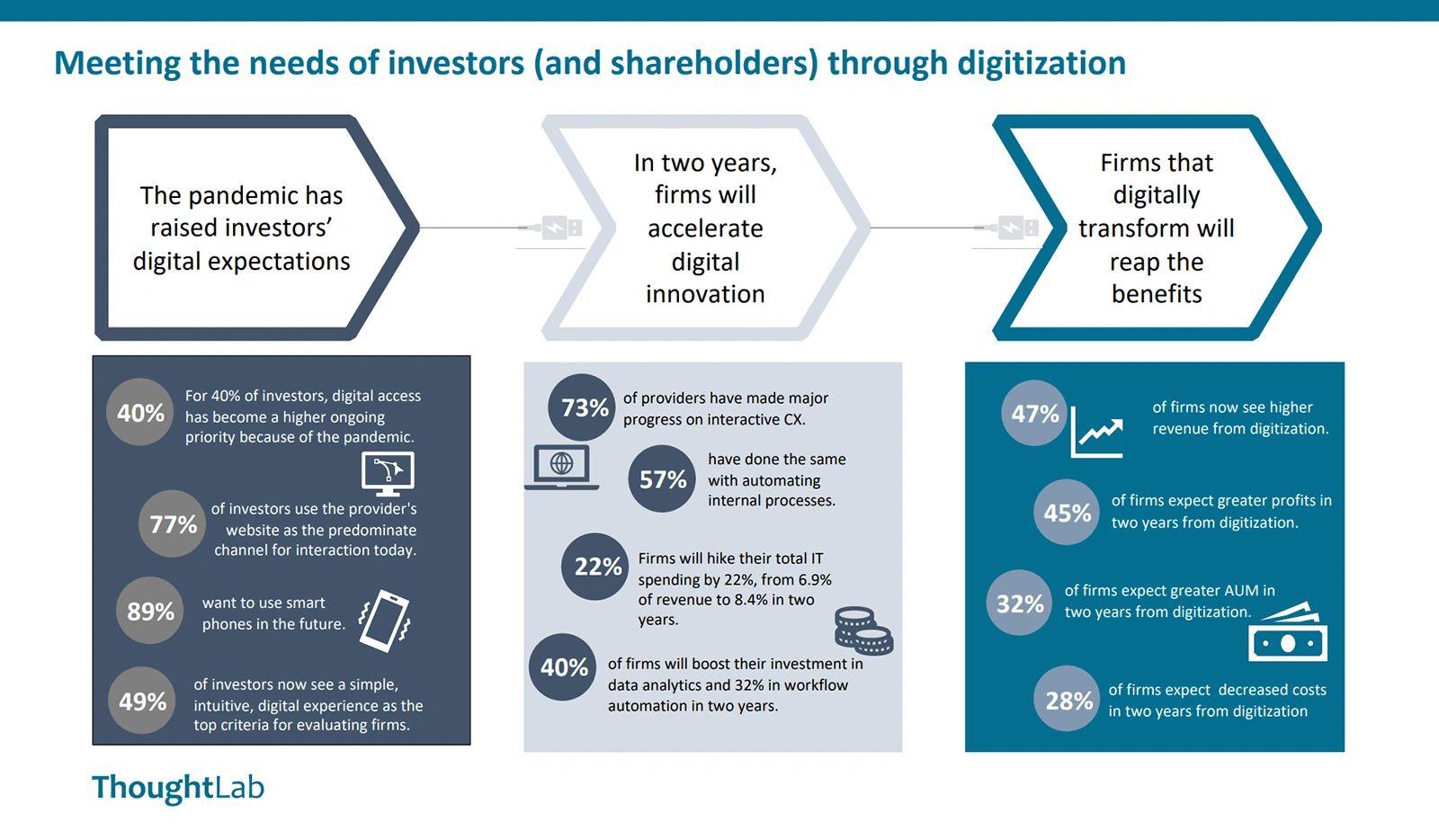

5. Digital transformation benefits wealth management firms and clients

The digital revolution is enabling wealth management firms to offer more personalized approaches and capabilities to their clients.

More than 85% of firms consider utilizing digital capabilities to serve clients a highly important goal.

This is directly in line with the wants and needs of investors.

A recent survey from ThoughtLab found that nearly 90% say their preferred channel for investment-related activity is mobile apps, and 75% of advisors say digital interactions will be the norm in two years.

Nearly 50% of firms are already seeing higher revenue from digitization.

Investment advisors are quickly turning their attention to wealthtech, the platforms, automation services, and other digital solutions that enable wealth management firms to provide advice and build relationships with their clients.

Multinational investment bank UBS used the pandemic to fast-track its digital transformation.

They launched the My Way tool, at an expense of $2.65 billion, to provide investors with a remote digital experience that includes onboarding, insights, and a connection to advisors through WeChat and WhatsApp.

The tool reportedly brought in $3.7 billion in its first year and could pull in up to $30 billion in the next year.

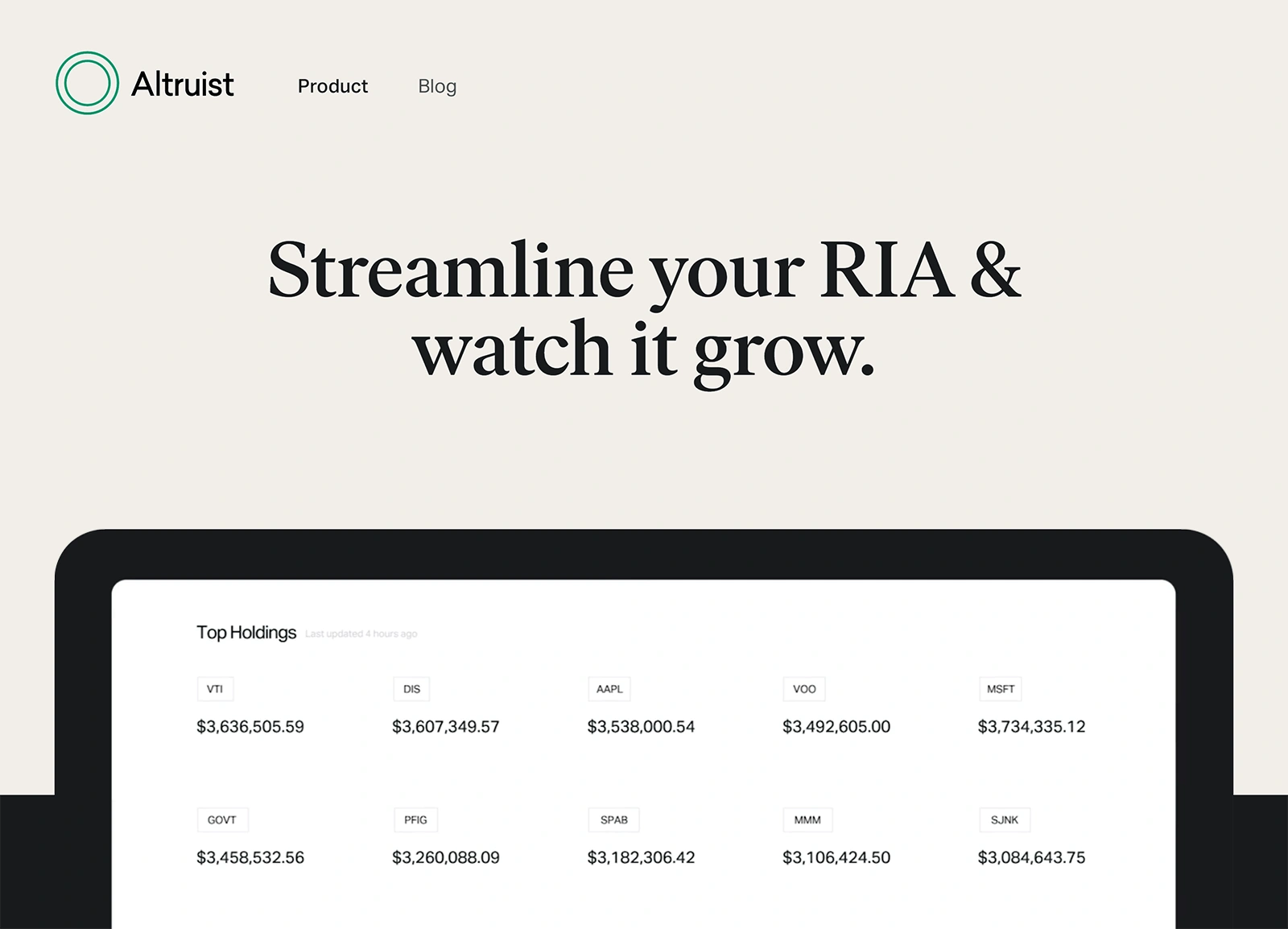

Altruist, a wealthtech startup formed in 2018, is a SaaS company serving RIA customers.

Its digital advising platform offers a portfolio management system, all-in-one reporting, automated model portfolios, and a client app.

It’s currently used by more than 1,000 financial planners.

Altruist offers streamlined software so that wealth advisors can spend more time focusing on best practices for their firms and achieving results for their clients.

In mid-2021, the company brought in $50 million worth of Series B funding from Vanguard, Venrock, and Insight Partners.

The wealth management firms that have successfully integrated the proper digital tools and resources are reaping the benefits.

Liferay reports that companies like this have experienced a 13% boost in productivity, an 8% increase in AUM (assets under management), and an 8% increase in revenue.

These benefits come from a variety of avenues like streamlined onboarding, on-demand reporting, sophisticated personalization, and AI investment advice.

Conclusion

That’s our list of the top six wealth management trends to watch over the course of the next two or three years.

As concerns about inflation and interest in cryptocurrency grow, watch for investors to start asking questions about alternative investment strategies.

We expect clients to demand that firms be able to handle new generations of investors and advisors. That means shifting priorities and building relationships in new ways. Those wealth managers who do so will be able to secure clients and keep them engaged with the digital solutions they crave.

Stop Guessing, Start Growing 🚀

Use real-time topic data to create content that resonates and brings results.

Exploding Topics is owned by Semrush. Our mission is to provide accurate data and expert insights on emerging trends. Unless otherwise noted, this page’s content was written by either an employee or a paid contractor of Semrush Inc.

Share

Newsletter Signup

By clicking “Subscribe” you agree to Semrush Privacy Policy and consent to Semrush using your contact data for newsletter purposes

Written By

Josh is the Co-Founder and CTO of Exploding Topics. Josh has led Exploding Topics product development from the first line of co... Read more