Get Advanced Insights on Any Topic

Discover Trends 12+ Months Before Everyone Else

How We Find Trends Before They Take Off

Exploding Topics’ advanced algorithm monitors millions of unstructured data points to spot trends early on.

Keyword Research

Performance Tracking

Competitor Intelligence

Fix Your Site’s SEO Issues in 30 Seconds

Find technical issues blocking search visibility. Get prioritized, actionable fixes in seconds.

Powered by data from

Latest Blog Posts

Featured Case Studies

See what's trending before everyone else

Each week, we'll send you our best Exploding Topics. Plus, expert insight and analysis.

9 Top Real Estate Trends In 2024

You may also like:

This report will examine the top nine trends impacting the real estate industry in 2024.

One of the key underlying drivers for these trends is a relocation from big cities to the suburbs.

But there are several other important changes in the real estate space to keep an eye on over the next 18-24 months.

With that, here are some of the most important real estate trends to know:

1. Home Prices Continue To Climb

Due to the increased demand for single-family homes and dwindling supply, prices for single-family homes have increased by 43% over the last 4 years.

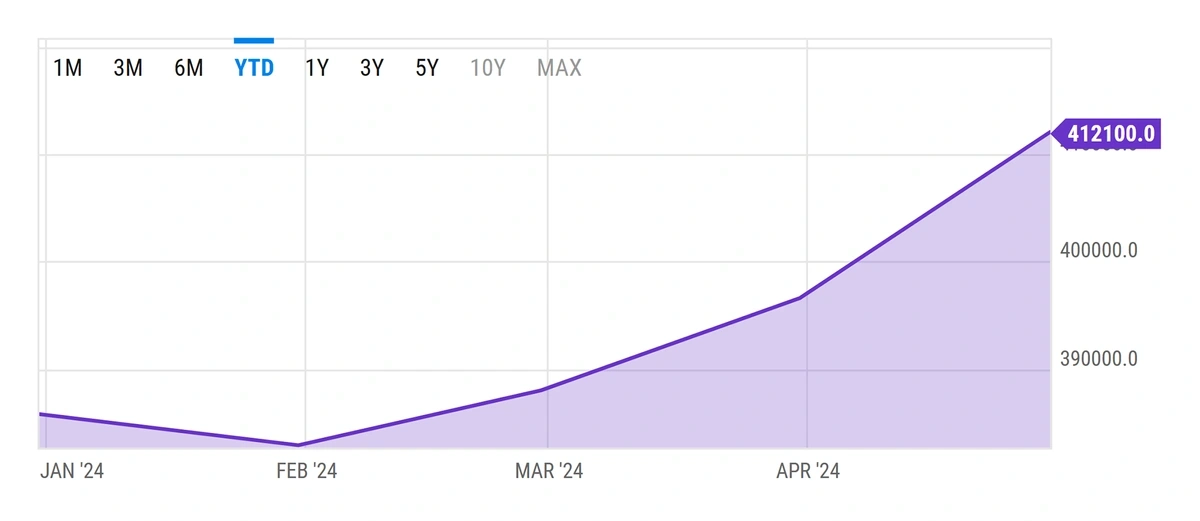

Average prices of single-family dwellings in the US have gone up by 7.6% just since January 2024

This trend is good for some but bad for others.

For existing home owners, they're seeing the equity in their homes increase substantially.

So, as market value increases, home equity does too.

In fact, the average US home owner saw a 9.6% increase in their equity last year alone, with a collective $1.5 trillion added.

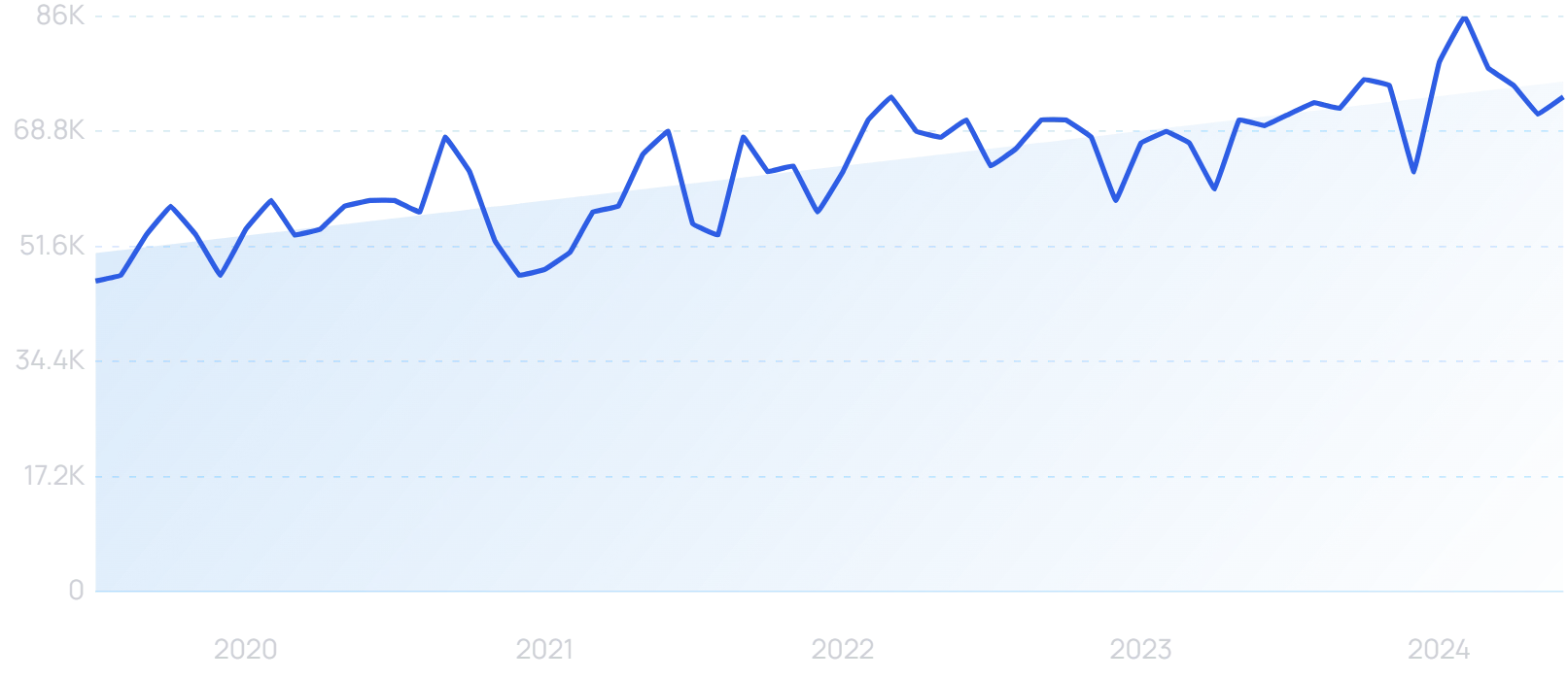

Online searches for "home equity" have steadily increased over the last decade.

But for first-time home buyers, high prices have largely locked them out of the housing market entirely.

However, it's worth noting that the housing market is showing some signs of cooling.

Median housing prices actually declined in the first quarter of 2024. As those who previously locked into low-rate mortgages reach the end of their terms, more property could come up for sale, potentially extending that trend.

That being said, it’s predicted that prices will continue to rise over the medium-term. Lawrence Yun, the chief economist at the National Association of Realtors, forecasts that the average sale price will rise by 15 to 25 per cent in the next five years:

“A crash happens with oversupply. It will not happen, because there isn’t enough inventory.”

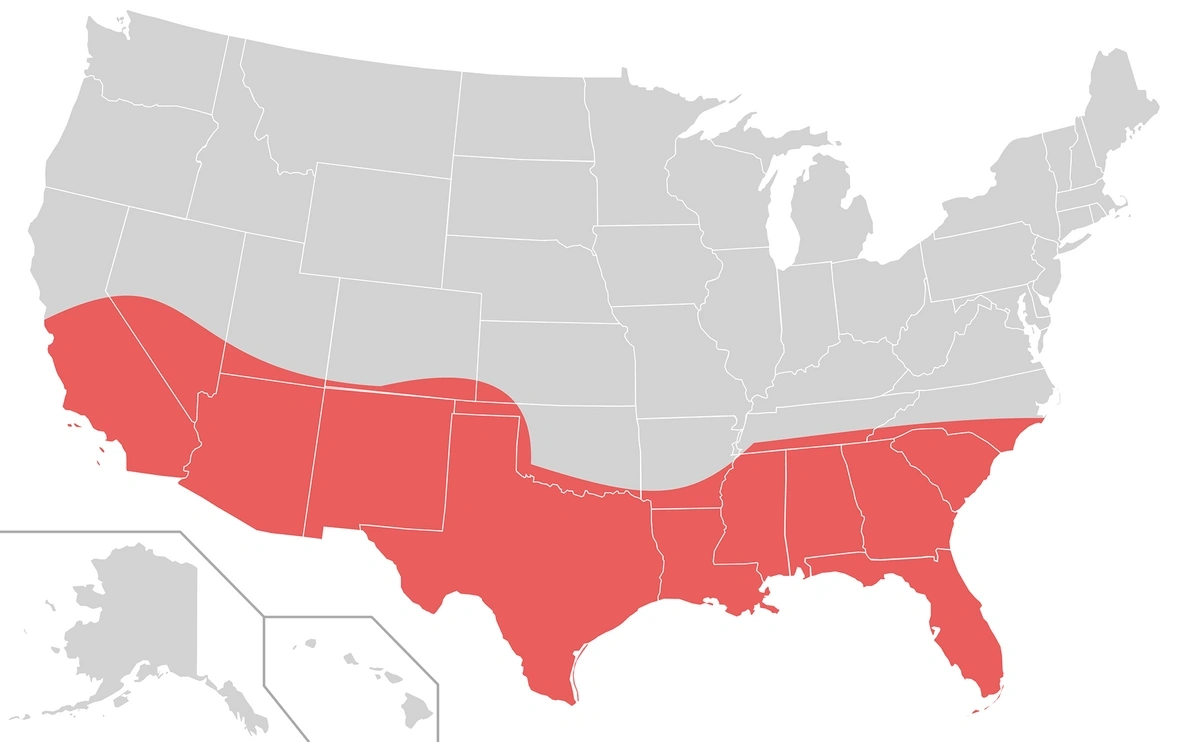

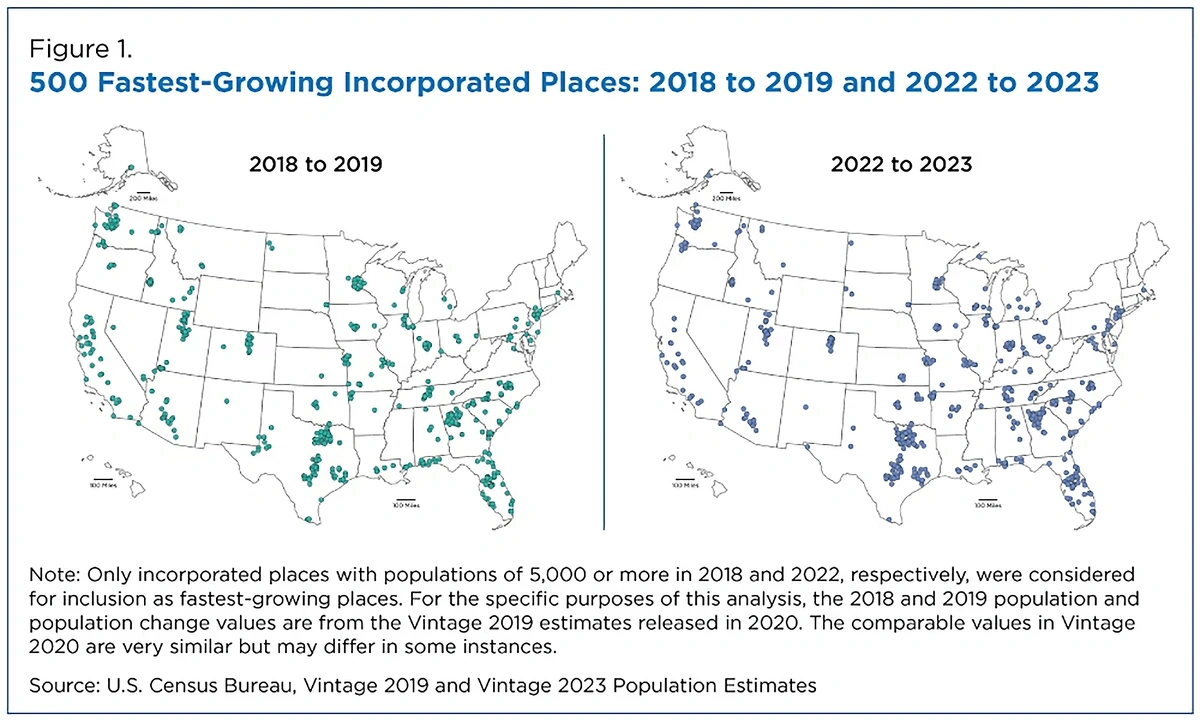

2. The Sun Belt’s Popularity Continues To Rise

As Americans shift out of big cities, one destination they are moving to is the Sun Belt.

The pandemic reinforced the increasing popularity of the Sun Belt, which is expected to persist for the foreseeable future.

The Sun Belt is the swath of the US that stretches from California to North Carolina and encompasses 18 southern states in between.

Approximately 80% of the country’s population growth has been concentrated in the Sun Belt states.

And according to one estimate, "The Sun Belt now holds about 50% of the national population (335 million), which is expected to rise to about 55% by 2040".

The Sun Belt is looking to see increased growth over the next 10 years.

As well as its appeal to the retired set, the region is also becoming increasingly more attractive to younger professionals due to lower taxes and more affordable housing prices and rent.

Additionally, even the biggest Sun Belt cities offer more space compared to the top US metro areas such as New York.

The growing relocation and rising population in the Sun Belt have bolstered real estate markets in the region.

The growth has not been limited to single-family homes but has also translated to multifamily housing and commercial real estate.

Two major Sun Belt metro areas, Dallas and Tampa, are ranked in the top ten US cities with the most real estate potential.

Other fast-growing cities (Austin in particular) are located in the Sun Belt region too.

On the other hand, major metropolitan areas, like New York, Philadelphia, and San Francisco are seeing fluctuating real estate demand. Around one in five San Francisco home owners are now selling their property for a loss.

3. House Hunting Goes Digital-First

The pandemic accelerated digitization across all sectors.

Searches for "digital transformation" are up 59% over the last 5 years.

And the real estate market is no exception.

Many buyers are now able to virtually tour property due to fresh innovations and advances in technology, such as:

- 3D Tours

- Drone videos

- Virtual staging

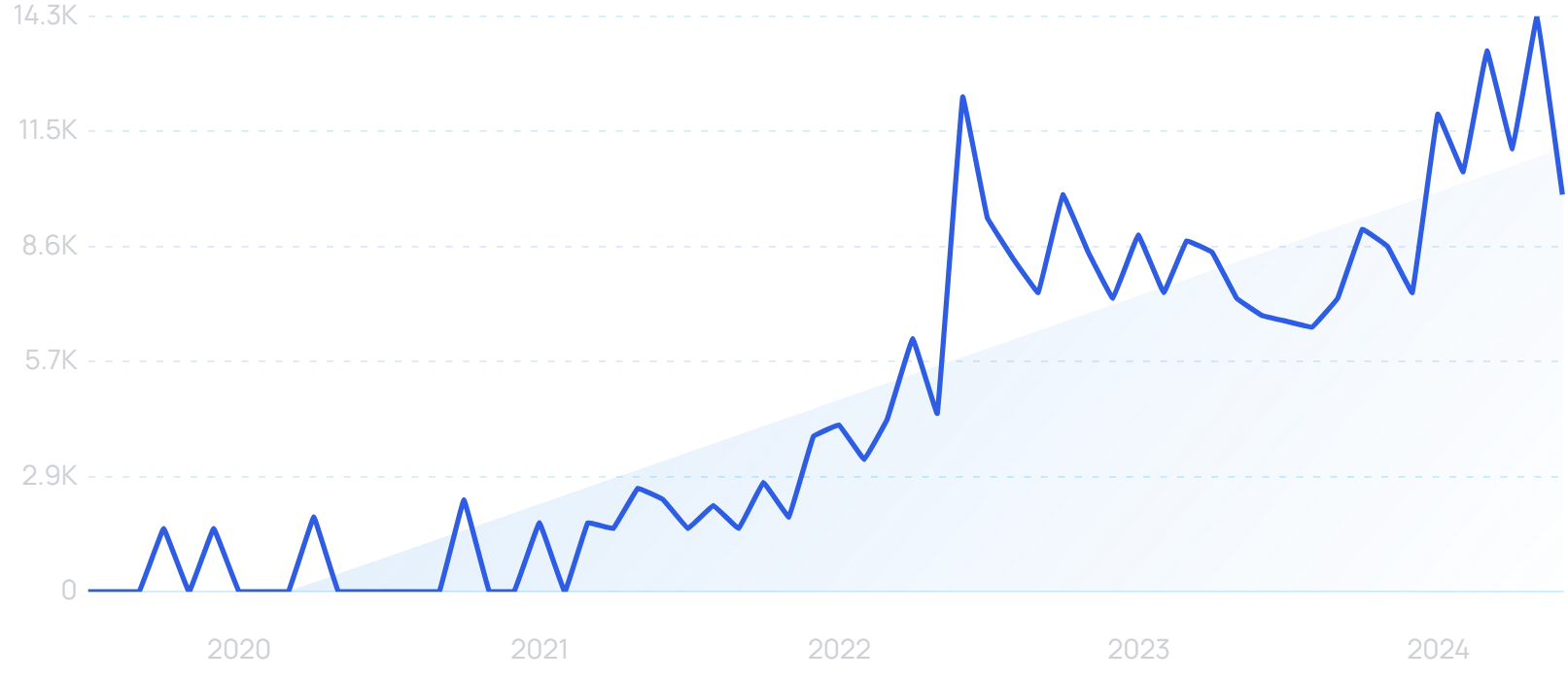

* Update chart *

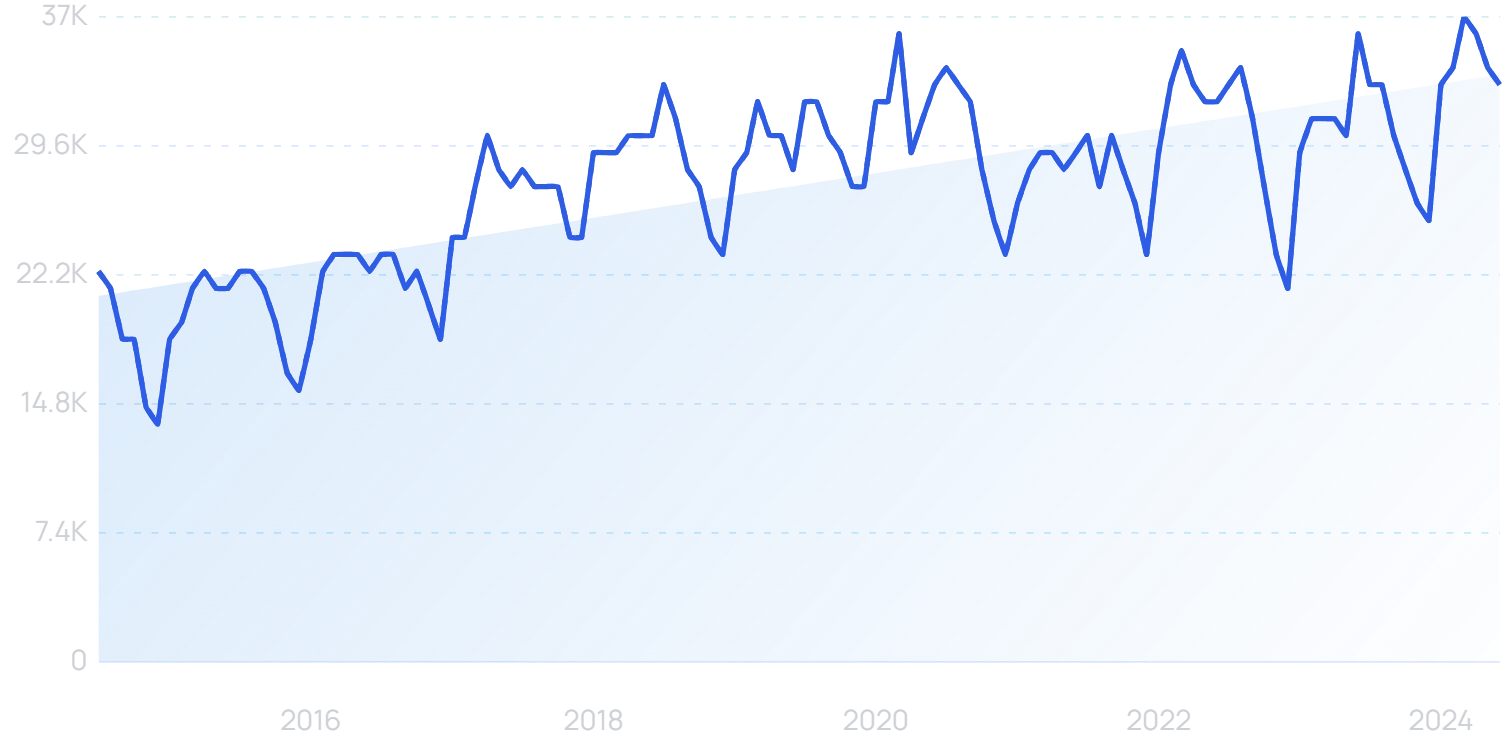

Searches for "virtual staging" are actually now higher than their pandemic peak.

Online searches for "virtual staging", which were on the rise pre-pandemic, shot up in 2020.

Notably, searches for virtual staging are actually significantly higher in 2024 (14,800 searches per month) than they were in 2020 (8,000 searches per month).

Online tools are now ubiquitous in property hunting. A National Association of Realtors report found that all buyers used the internet in the search process, with looking online the first step for 41% of people.

Online tools are now the go-to starting point for more than 4 in 10 people looking to buy property.

Getting a mortgage can be done online now too.

Huspy has initially focused on the UAE market. It allows users to search for a property and compare financing options all in one place, and has raised $37 million in Series A funding.

Online searches for "Huspy” have climbed rapidly since it was founded.

Millennials, who are notorious for their reliance on social media, are also turning to technology to learn more about their new neighborhoods.

Websites like Nextdoor allow residents of a particular area to stay in touch with other locals and keep up with neighborhood events.

4. Americans Move From Cities To The Suburbs

While the shift has slowed since the height of the pandemic, Americans are still moving to the burbs in droves.

In fact, the US Census Bureau reports that Americans are continuing to move to smaller cities and the suburbs.

The US population is shifting away from urban centers and towards smaller cities and towns.

The two underlying reasons for the shift are necessity and choice.

Those who cannot afford to stay are moving out of necessity.

While the wealthy are relocating by choice.

Notably, the rise of remote work means that it's no longer a requirement to live and work in a big city.

Last but not least, the suburbs are an attractive destination due to lower taxes and cheaper housing and rent prices.

Some who are moving out of big cities are looking for suburbs that retain some of the big city feel, areas that urban planner Daniel Parolek refers to as “middle neighborhoods”.

While the predominant feature of “middle neighborhoods” is the single-family home, these areas also retain some of the conveniences of a big city, such as multifamily housing options, good public transportation, high walkability scores, shopping, and restaurants.

According to Parolek, “middle neighborhoods” are difficult to construct from a regulations perspective, but perhaps this will start to change in the future as demand for such areas increases.

The shift from cities to suburbs is also driving some of the other real estate trends on this list.

Such as the increasing popularity of the Sun Belt, rising median home prices, and an overall housing shortage.

5. Single-Family Housing Demand Creates Shortages

The migration from cities to suburbs is resulting in growing buyer demand for single-family homes.

However, supply doesn't appear to be catching up with demand.

Since 2012 there's been a gap of over 7 million single-family homes.

New households outnumber new homes by more than 7 million since 2012.

In order to meet demand, the current pace of building would need to triple.

The demand for houses is compounded by another coinciding trend: Millennials entering the home ownership phase of their lives.

Millennials looking to purchase their first house or start a family are also spurring suburban growth.

As a result, single-family housing inventory remains at historic lows.

(The supply issue is exacerbated by the fact that institutional investors are buying approximately 8% of all homes on the market).

However, the market is projected to eventually stabilize. And the pace of new construction may catch up with the increased demand. In May 2024, privately-owned housing completions were up 1% year-on-year.

The housing shortage coupled with rising housing prices has been a boon for management and construction companies.

6. Multi-Generational Living Is On The Rise

Undoubtedly influenced by the squeeze on supply and rising prices, multi-generational living has become far more commonplace than it once was.

Between 1971 and 2021, the number of people living in multi-generational households in the US quadrupled.

There’s a similar trend in the UK, where the latest census data showed a 14.7% increase in adult children living with their parents over the last 10 years.

But it’s not just a case of children being unwilling or unable to move out due to the spiralling costs. More people are also living with elderly parents, in households that can span three or more generations.

18% of people in the US aged 65 or over are in multi-generational households.

It’s a trend also influenced by immigration, with 26% of Black and Hispanic Americans in a multi-generational living setup, and only 13% of White Americans.

7. Mortgage Rates See No Signs Of Dropping

At the beginning of January 2021, mortgage rates hit a record low of 2.65%.

This caused a spike in mortgage applications.

However, in an effort to combat inflation, interest rates have seen multiple increases over the last few years.

The average 30-year fixed rate jumped to 7.08% in October 2022, and that figure has remained around 7% into 2024.

This sudden increase in interest rates made buying a home more expensive. And increased monthly mortgage payments for those with variable mortgages.

Looking ahead, the Fannie Mae Housing Forecast predicts that “We revised our mortgage rate forecast downward slightly month over month. We now forecast the 30-year fixed rate mortgage rate to average 6.6% in 2024, and to average 6.1% in 2025.”

Other experts do predict rate drops over the next 12 months.

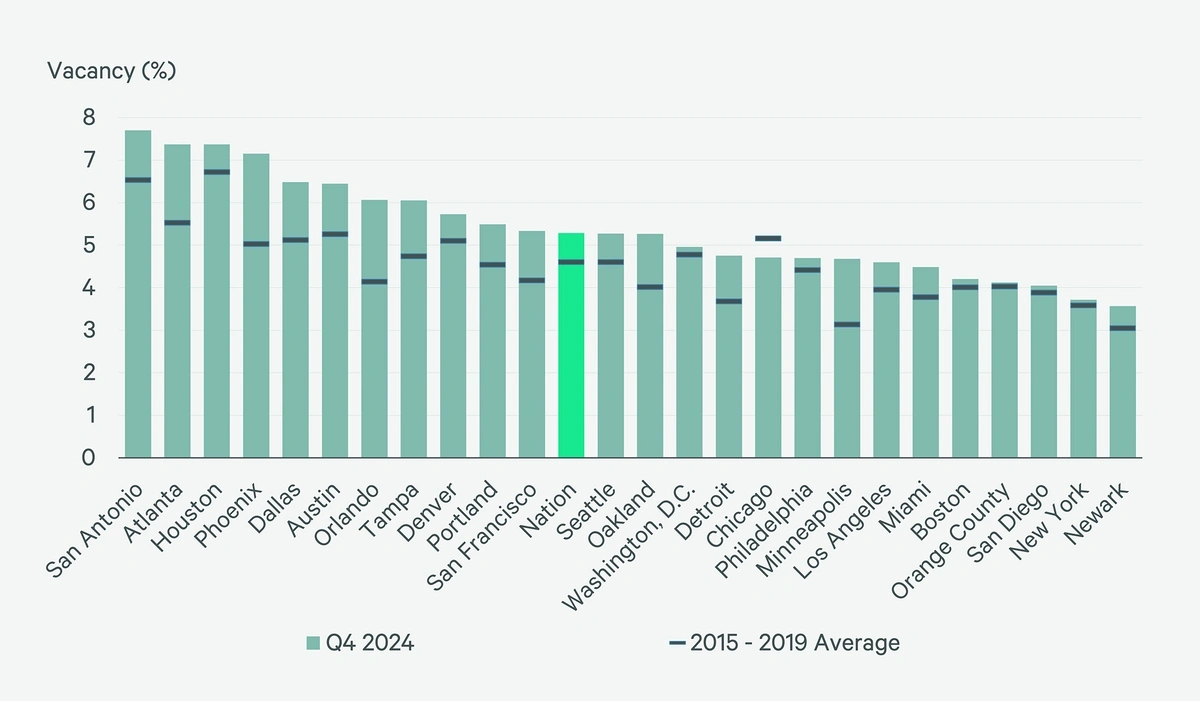

8. Rental Property Market Declines

Partly due to the shift of people from cities to suburbs, the rental market for both residential and commercial properties in big cities is on a slight decline.

According to Zillow, overall rental price growth has settled down to around 0.4% month-over-month. That peaked at 0.79% from August to September 2022.

Demand for rental properties will likely continue to decline in the biggest cities. People who can afford it look to buy a house. Those who cannot do so look for other alternatives (like staying with their parents) to save money.

Rental vacancies are duly increasing in major metropolitan areas. Charleston, Memphis, Houston and Oklahoma City all have vacancy rates above 10%, placing them in the nationwide top 10.

However, demand for rental properties is actually going up in mid-size and smaller cities around the country as the demand for homes in these areas outpaces the supply. Experts have noted this growth in secondary markets.

The downturn in the rental market is creating real estate investment opportunities.

Investors can also take advantage of commercial properties, such as hotels and retail buildings, and repurpose them into housing units.

9. Commercial Real Estate Landscape Remains In Flux

Office vacancies rose to 19.6% in Q4 2023, the highest on record and the largest quarterly surge since the start of 2021.

Commercial real estate has been fundamentally impacted by changing working patterns.

It’s important not to overstate the shift to remote work when it comes to the commercial real estate market.

70% of Americans still prefer a working arrangement fully or mostly in person, a figure that actually rises among those aged 18-34, whose early working experiences were shaped by the pandemic.

But nor can the lasting effects of Covid be ignored. Commercial real estate opportunities trending in a more positive direction come in the form of retail and multi-family properties.

Tom LaSalvia, Head of Commercial Real Estate Economics at Moody's Analytics CRE, says “Year over year, national level effective rent for neighborhood and community shopping centers is the highest it has been since before the onset of the pandemic in early 2020.”

And while delivery of an estimated 440,000 new multi-family units in 2024 is expected to slow growth in this sector, construction starts have already dropped by more than 50% from their Q1 2022 peak.

Construction of new multi-family units is declining steeply

Conclusion

That wraps up our list of important real estate trends happening right now.

As more people move to the suburbs and look to purchase a home, single-family housing prices are expected to stay high and supply low.

High mortgage rates may hurt demand for homes, with inter-generational living among the alternatives being sought.

In the meantime, the rental property market in large cities will remain in decline, which will provide opportunities for real estate investors planning for a post-pandemic recovery of city life.

Well-placed retail establishments are already benefiting from the green shoots of this recovery, although effects on commercial office space are proving more long-lasting.

Stop Guessing, Start Growing 🚀

Use real-time topic data to create content that resonates and brings results.

Exploding Topics is owned by Semrush. Our mission is to provide accurate data and expert insights on emerging trends. Unless otherwise noted, this page’s content was written by either an employee or a paid contractor of Semrush Inc.

Share

Newsletter Signup

By clicking “Subscribe” you agree to Semrush Privacy Policy and consent to Semrush using your contact data for newsletter purposes

Written By

Josh is the Co-Founder and CTO of Exploding Topics. Josh has led Exploding Topics product development from the first line of co... Read more